Table of Contents

Key Takeaways

- Effective law firm bookkeeping requires daily transaction logging and strict separation of client trust funds from general operating accounts.

- Consistent monthly three-way reconciliations are essential to ensure bank balances, client ledgers, and trust liability accounts match perfectly.

- Detailed client ledgers and precise matter coding protect your practice from compliance pitfalls and potential bar association audit issues.

- Professional accounting services and specialized legal software streamline financial tasks, allowing lawyers to focus entirely on their billable work.

What is Law Firm Bookkeeping?

Law firm bookkeeping means logging every dollar in and out daily. Do not confuse it with analysis or tax strategy, it is pure data entry with strict rules. In law firm accounting, every transaction ties to a specific client and matter code. This matters because the bar audits randomly. If your legal bookkeeping is messy, you get flagged. Also, accounting for law firms requires understanding IOLTA rules that general bookkeepers often overlook.

Law firm bookkeeping catches 30% of bar audit issues before they become ethics violations. Because financial mismanagement is one of the quickest ways to lose a license, staying aligned with the American Bar Association’s Model Rules of Professional Conduct regarding client property is non-negotiable.

As seen commonly, solo lawyers usually handle bookkeeping for law firms between court dates, whereas paralegals enter data in mid-sized practices. Some firms also hire professional virtual accounting services from specialists to ensure the books stay audit-ready without draining internal resources. In short, to each their own.

The work of bookkeeping is very repetitive but critical. You have to record payments, log expenses, and match statements. If law firm bookkeeping is done right, it means you know the money you are earning and exactly how much client money you hold. In case it’s done wrong, you might end up borrowing from Peter to pay Paul without realizing it. Let’s figure out the things you need to keep in mind, as a legal expert, to make this process smooth and less cumbersome.

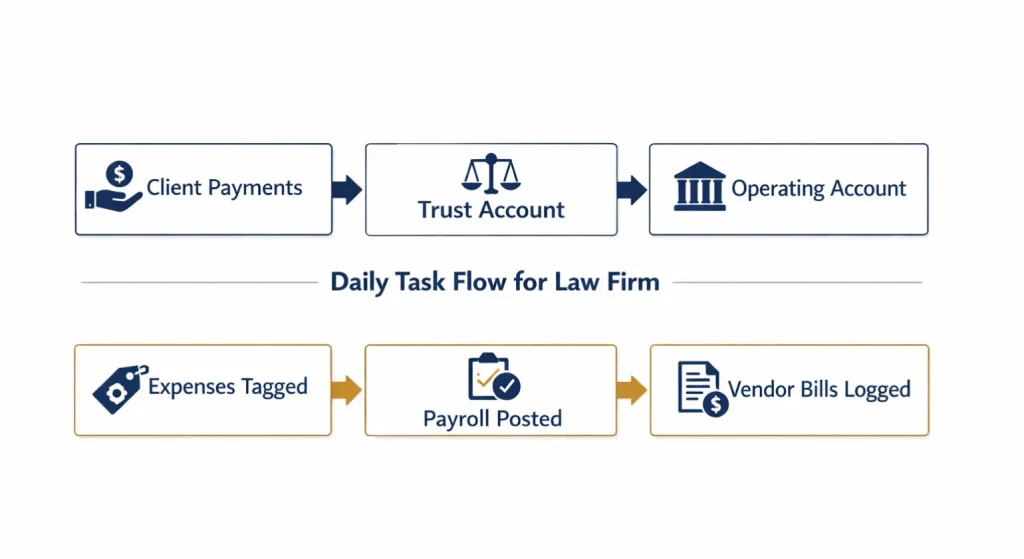

1. Core Daily Tasks Under Legal bookkeeping

Starting the process, client payments hit your inbox daily. Enter them immediately with client and matter tags. Law firm accounting requires retainers go to trust. Fees for completed work go to operating. Then, settlements are split between liens, fees, and client proceeds. During busy days and slow recording, expenses pile up fast, office supplies hit operating, and client costs like court filing fees get tagged as reimbursable.

To manage that effectively, it is advised to do payroll entries weekly where you post staff wages and withholdings. Do not guess at numbers. Use payroll reports from Gusto or ADP, and follow IRS guidelines on employment taxes to ensure accuracy. Accounting for law firms uses basic posting only, though tax filings are for accountants later.

Vendor payments need recording when checks are cut or wires are sent. So, log the invoice first, then the payment. Bookkeeping for law firms requires matching so accounts payable stays clean. If you pay a process server, tag it to the client matter immediately.

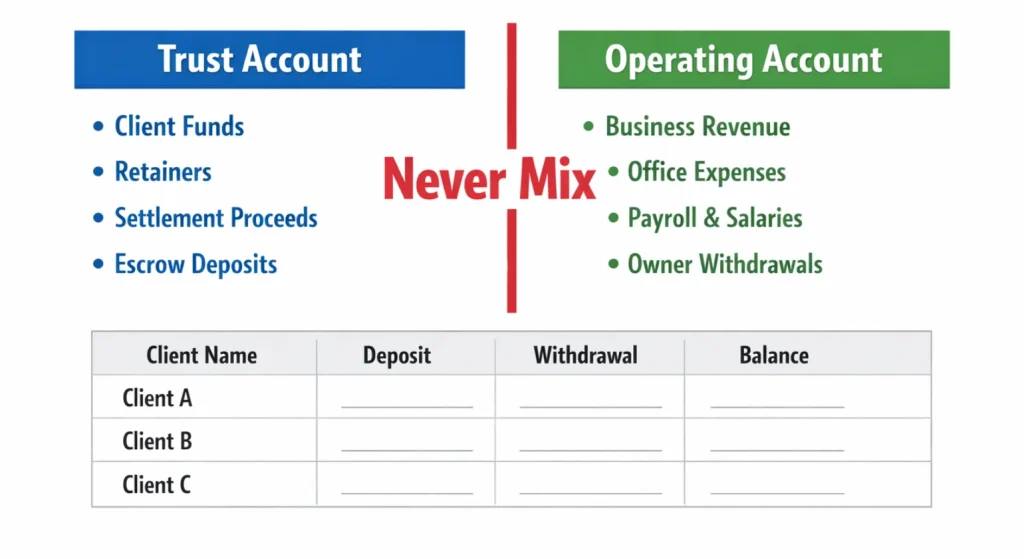

2. Trust Account Bookkeeping Fundamentals

FYI, IOLTA rules are quite simple but strict. For example, your client funds never mix with firm funds. Accurate law firm bookkeeping separates your money for rent from client money for case expenses. Keep them in separate bank accounts. You can find specific state variations on these requirements at IOLTA.org.

Every client should get an individual ledger. This is not optional in law firm accounting. Let’s learn it with a scenario. If you hold money for Smith, you track Smith’s balance separately from Jones. When you deposit a retainer, it goes on Smith’s ledger. When you pay a medical record fee, it comes off Smith’s ledger.

Retainer tracking requires precision. For example, when a client sends $5,000, you post the deposit to trust, and suppose you bill $2,000 for work. The next step is that client should get the invoice. Legal bookkeeping rules say transfer from trust to operating only after they approve the bill. Never move money before billing.

Here is a simple trust ledger example for a personal injury case showing proper law firm bookkeeping:

Trust Entry Type | Description | Client/Matter Code Example |

Retainer Deposit | Client advance for costs | Miller-PI-2026 |

Medical Records | Copy service fee | Miller-PI-Exp-01 |

Expert Witness | Deposition prep payment | Miller-PI-Exp-02 |

Fee Transfer | Earned fees post-billing | Miller-PI-Fee-Transfer |

The math must balance. Opening balance plus deposits minus withdrawals equals closing balance. Accounting for law firms demands finding errors before Friday.

3. Billing and Accounts Receivable Logging

Invoices go out monthly for most firms. When you bill, post the entry to accounts receivable. Debit AR, credit fee income. Law firm bookkeeping means if you billed for costs advanced, credit the client cost account.

Payments arrive and need matching. Client pays $3,000 on a $3,500 invoice. Post the payment to that specific invoice. Leave $500 open. Legal bookkeeping requires applying payments to specific matters, not oldest invoices automatically.

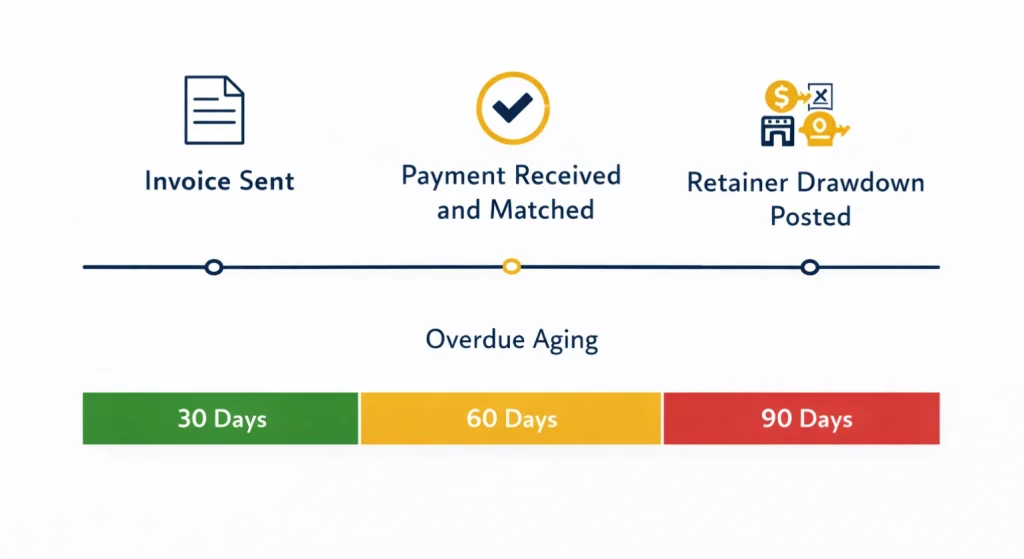

Aged AR reports show who owes money. Run it weekly. Categorize by 30, 60, and 90 days past due. Law firm accounting without aged AR means cash flow problems. If you do not log invoices right, you cannot age them right.

Retainer drawdowns happen after billing. Post a journal entry transferring funds from trust payable to operating income. This must tie to the invoice. If invoice #1010 is for $2,000, the drawdown is $2,000 in proper law firm bookkeeping.

4. Bank and Credit Card Reconciliations

Reconcile monthly. No exceptions. Match your book transactions to bank statements line by line. Start with operating account. Law firm accounting requires clearing every check and deposit. Uncleared items from three months ago need investigation.

Trust reconciliation is harder. A three-way match is required. The bank statement balance equals total of all client ledgers equals your trust liability account balance. Legal bookkeeping stops everything if these three numbers differ.

Common reconciliation checklist items for law firm bookkeeping:

- Verify all deposits match bank statement dates and amounts.

- Flag any discrepancy under $5 but investigate anyway.

- Document adjustments with memos explaining why.

- Check for bank fees on trust accounts, these come from operating, never trust.

- Confirm negative client balances do not exist.

Negative trust balance means you spent client money you did not have. This is a compliance violation in law firm accounting. Fix immediately. As many firms utilize outsourced legal support to handle these granular reconciliations to ensure no detail is missed, you can consider this option too.

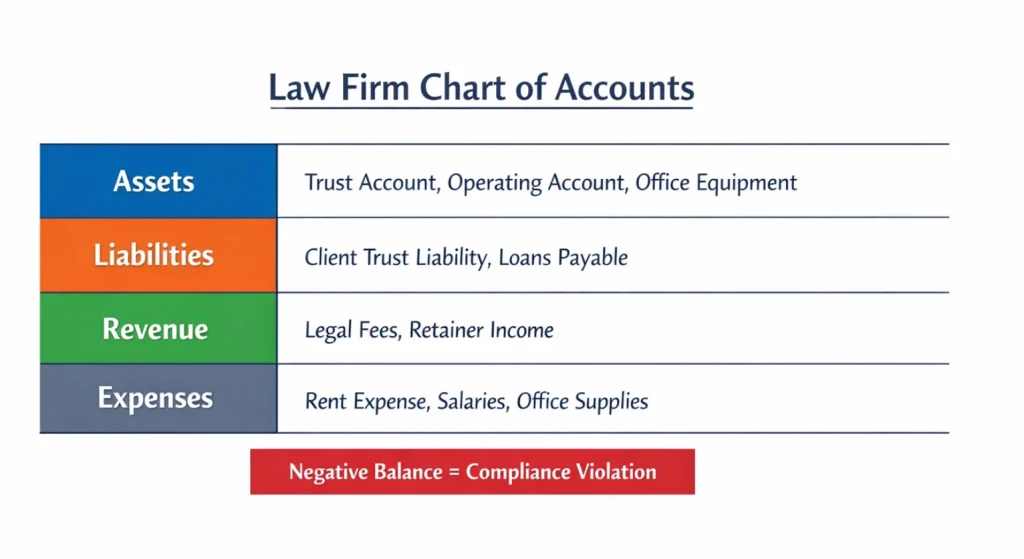

5. Setting Up Your Chart of Accounts

Chart of accounts organizes everything. Start with assets: operating bank, trust bank, accounts receivable, undeposited funds. Add liabilities: trust payable, credit cards, loans for proper legal bookkeeping.

Revenue accounts need specificity. Create separate accounts for contingency fees, hourly billing, flat fees, and retainers. Law firm accounting benefits from this later when analyzing profitability.

Expenses get broken out. Bar dues, CLE costs, client meals, expert witnesses, court filing fees. Client meals belong in client costs, not general marketing in law firm bookkeeping.

Add law firm-specific accounts for proper accounting for law firms:

- Client Advances: money you spend on cases before reimbursement.

- Unbilled Costs: expenses incurred but not yet invoiced.

- Matter Expenses: detailed tracking per case.

Here is a sample abbreviated table showing law firm accounting categories:

Account Type | Examples |

Current Assets | Operating Bank, Trust Bank, Accounts Receivable, Undeposited Funds |

Liability | Trust Payable, Credit Card Payable, Loans |

Revenue | Contingency Fees, Hourly Billing, Flat Fees, Retainer Income |

Expenses | Bar Dues, CLE Registration, Client Meals, Expert Witness Fees, Legal Research |

6. Weekly and Monthly Bookkeeping Checklist

Weekly tasks keep law firm bookkeeping manageable. Enter prior week’s transactions every Monday. Run AR aging to see who is late. Review uncategorized bank feed items. Tag them to clients immediately.

Monthly tasks dig deeper for proper law firm accounting. Full reconciliation of all accounts by the 5th. Review every client ledger for negative balances. Print backup reports and store digitally. Sign off on three-way trust reconciliation.

Printable checklist template for legal bookkeeping:

- Day 1: Post all bank feeds from prior month.

- Day 2: Match invoices to payments received.

- Day 3: Review trust ledger for anomalies.

- Day 5: Run financial statements for partner review.

- End of Month: Three-way recon sign-off with documentation.

7. Tools for Streamlined Law Firm Bookkeeping

We have listed a few tools that would work best for your legal bookkeeping needs.

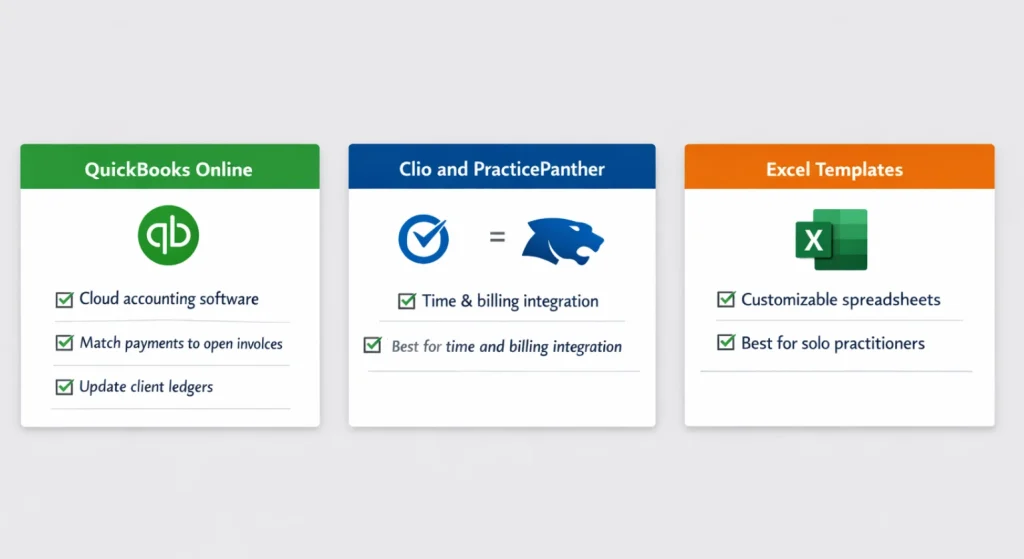

- QuickBooks Online works for most firms needing law firm accounting. Set up trust sub-accounts properly. Use classes for practice areas and locations. Many lawyers search QuickBooks for lawyers specifically.

- Clio and PracticePanther integrate time tracking with billing. Time entries flow to invoices automatically. This legal bookkeeping integration reduces data entry errors.

Law firm accounting services often use specialized tools. Excel templates help solos start cheap. Simple ledgers track trust balances. Reconciliation templates catch math errors for accounting for law firms.

Conclusion and Next Steps

Compliant law firm bookkeeping protects your license and peace of mind. Daily entries prevent month-end chaos. Monthly reconciliations catch errors early. Trust ledgers keep client money safe. Legal bookkeeping done right means sleeping soundly during bar audits.

If bookkeeping eats your billable hours, you can contact us for specialized law firm accounting services. Let us handle the numbers while you handle the law.

That being said, if you still want to know more about bookkeeping for lawyers or other aspects of operations related to law firms, we have curated two informative reads below.

In case you are interested to Read More? Check Out >>> Google Ads for Lawyers: Beginner to Advanced Strategies guide

You can also Read >>> Smarter Managed IT Services for Law Firms: 2026 Guide

FAQs

1. What is the difference between law firm bookkeeping and accounting?

Law firm bookkeeping focuses on the daily recording of financial transactions, such as logging costs and deposits. Law firm accounting involves analyzing that data for tax strategy, financial health, and long-term business growth. Bookkeepers record, while accountants interpret.

2. How often should I reconcile my IOLTA account for proper legal bookkeeping?

You should reconcile your IOLTA account at least monthly to remain compliant with bar associations. However, high-volume practices often perform weekly reconciliations in their law firm accounting to catch errors early and ensure every client’s ledger remains perfectly accurate.

3. Can I use QuickBooks for law firm accounting?

Yes, QuickBooks is effective for law firm bookkeeping if configured correctly. You must establish a specific trust liability account and ensure it matches individual client ledgers. Many firms integrate it with legal software to streamline specialized trust tracking and compliance.

4. What happens if my trust account does not reconcile in law firm bookkeeping?

You must stop all trust activity immediately to prevent ethics violations. In law firm accounting, you must locate the discrepancy before moving any more money. If a negative balance occurs, you may need to deposit firm funds to correct it.

5. Do I need separate bank accounts for each client in accounting for law firms?

No, a single IOLTA account typically holds all client funds. However, law firm accounting requires maintaining individual ledgers for every client to track their specific balances. The key is ensuring these funds never commingle with your firm’s daily operating capital.